Navigating the optimal mix of salary and dividends is one of the most impactful financial decisions you can make as a limited company director. Getting it right minimises your overall tax liability, preserves cash flow, and ensures compliance.

This definitive guide for the 2025/26 tax year breaks down the latest HMRC thresholds and National Insurance changes to provide a clear, actionable strategy for paying yourself tax-efficiently.

Executive Summary: The Optimal Strategy at a Glance

For most director-shareholders, the most tax-efficient approach remains a combination of a low salary and the balance in dividends. The ideal salary level, however, depends critically on your company’s employment structure.

The Golden Rule: Extract a salary up to your Personal Allowance without incurring personal National Insurance, while maximising the corporation tax deduction for the company.

🏆 The Global Forum Recommendation

For most directors in 2025/26, we recommend:

- A salary of £12,570 (utilising your full Personal Allowance).

- The remainder of your income as dividends.

The key exception: If you are a sole director with no other employees, a lower salary may be marginally more cash-flow efficient, though sacrificing state pension credits.

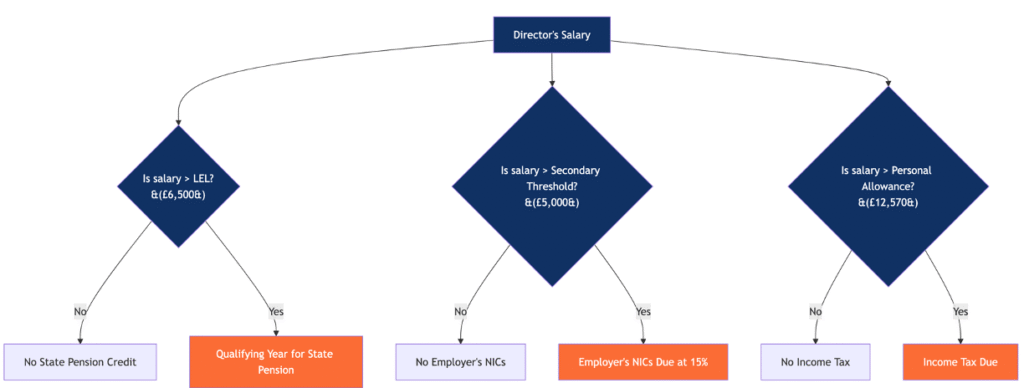

Understanding the 2025/26 Tax Landscape: Key Thresholds

Your strategy is built upon four critical government thresholds. The following visual roadmap shows how they interact.

The Official HMRC Figures for 2025/26:

- Personal Allowance: £12,570 (Earnings below this are free from Income Tax). [Source: HMRC PN 1, Dec 2024]

- Employer NICs Secondary Threshold: £5,000 (Earnings above this incur 15% Employer NICs). [Source: HMRC EPN 1, Dec 2024]

- Lower Earnings Limit (LEL): £6,500 (Earnings above this qualify you for a State Pension credit, even if no NICs are paid). [Source: HMRC EPN 1, Dec 2024]

- Employment Allowance: £10,500 (Available to most businesses with more than one employee). [Source: HMRC EPN 1, Dec 2024]

Your Customised Strategy: Scenario-Based Analysis

The best path for you depends entirely on whether your company can claim the Employment Allowance.

Scenario 1: Sole Director with No Other Employees

If you are the only person on the company payroll, you are generally not eligible for the Employment Allowance. This changes the calculus, giving you three primary options.

Option A: The Minimalist (£5,000 Salary)

Best for: Directors prioritising absolute minimal payroll admin and immediate cash flow.

Tax Impact: No Income Tax, no NICs of any kind.

The Trade-off: You do not secure a qualifying year for your state pension.

Option B: The State Pension Qualifier (£6,500 Salary)

Best for: Directors seeking the cheapest way to protect their state pension entitlement.

Tax Impact: No Income Tax. Employer NICs due: £225 (£1,500 * 15%).

The Benefit: Your salary is above the LEL, so you receive a full state pension credit.

Option C: The Full Allowance Utiliser (£12,570 Salary)

Best for: Directors focused on maximising the company’s corporation tax saving.

Tax Impact: No Income Tax. Employer NICs due: £1,135.50 (£7,570 * 15%).

The Net Benefit: While you pay £1,135.50 in NICs, the company saves £1,654.05 in Corporation Tax (£8,705.50 total additional expense * 19%). This creates a net saving of £518.55 for the company.

Global Forum Insight: For sole directors, Option B (£6,500) is often the most balanced choice, protecting your state pension at a low cost. However, if your company’s profits are healthy, Option C (£12,570) generates a net tax saving, making it the most efficient long-term strategy.

Scenario 2: Multiple Directors or Additional Employees

If your company has at least two directors on payroll, or one director and another employee, you can likely claim the £10,500 Employment Allowance. This fundamentally changes the strategy.

✅ The Recommended Strategy: £12,570 Salary

- With the Employment Allowance, the Employer NICs on salaries of £12,570 are fully covered.

- Result: You extract a salary that uses your full tax-free Personal Allowance, secure your state pension credit, and incur no Income Tax or NICs.

- The company receives a full corporation tax deduction for the salary without the burden of an NICs bill.

This is unequivocally the most tax-efficient position for both you and your company.

Why the Salary & Dividend Mix is So Effective

This strategy leverages the strengths of both payment methods while mitigating their weaknesses.

The Role of Salary

- Corporation Tax Relief: Salaries are a deductible business expense, reducing your company’s profit and its Corporation Tax bill.

- Preserves State Benefits: A salary above the Lower Earnings Limit secures your National Insurance record for the state pension.

- Uses Personal Allowance: It utilises your £12,570 tax-free allowance, which would otherwise be wasted.

The Role of Dividends

- Lower Tax Rates: Dividend tax rates (0%, 8.75%, 33.75%, 39.35%) are lower than income tax rates (20%, 40%, 45%).

- No National Insurance: Dividends are not subject to National Insurance, saving you and your company 15% in Employer NICs.

- Tax-Free Allowance: You have a £500 Dividend Allowance (2025/26) before tax is due.

Critical Considerations & Professional Advice

Profit is King: This strategy assumes your company has sufficient profits to cover the salary and dividends. Dividends can only be paid from post-tax profits.

Formal Procedures: Dividends must be properly declared via board meetings and dividend vouchers to be HMRC-compliant.

Personal Circumstances: If you have other sources of income, a student loan, or are claiming Child Benefit, your optimal strategy may differ.

Changing Laws: The tax landscape is constantly shifting. The reduction in the Dividend Allowance and changes to NICs underscore the need for ongoing professional advice.

How Global Forum Consulting Ltd Can Help

As your strategic partner, we move beyond simple compliance to deliver optimal tax efficiency.

- Personalised Director Remuneration Strategy: We analyse your specific circumstances to model the perfect salary-dividend split for you and your company.

- Phttps://globalforumconsulting.com/payroll/ayroll & Compliance Management: We set up and manage your payroll, ensuring your salary is processed correctly, RTI submissions are filed, and all NICs are calculated accurately.

- Dividend Administration: We ensure your dividend declarations are legally sound and fully documented, protecting you from HMRC challenges.

- Holistic Tax Planning: We integrate your remuneration strategy with your wider financial goals, including profit retention, pension contributions, and long-term exit planning.

Final Recommendation

For the 2025/26 tax year, the evidence is clear:

- If you have multiple employees/directors: Pay a salary of £12,570 to fully utilise the Employment Allowance and your Personal Allowance.

- If you are a sole director: A salary of £12,570 is still likely the most tax-efficient, though a salary of £6,500 is a prudent alternative if you wish to minimise upfront NICs while protecting your state pension.

Don’t leave your personal wealth to chance. A poorly planned remuneration strategy can cost you thousands.

Ready to Optimise Your Director’s Pay?

Let Global Forum Consulting build you a tailored, tax-efficient blueprint that works as hard as you do.

Contact Us for a Personalised Review*This article is based on current legislation for the 2025/26 tax year and is for general guidance only. Specific advice should be sought for your individual circumstances. All HMRC thresholds have been validated against official government announcements as of December 2024.*